New in the Letitia Files: Did New York AG Letitia James Commit Insurance Fraud, Too? It Looks Like It

Guest post by Joel Gilbert

In the Gateway Pundit, I recently documented how Letitia James misrepresented the number of apartment units in her apartment building when applying for loans and refinancing.

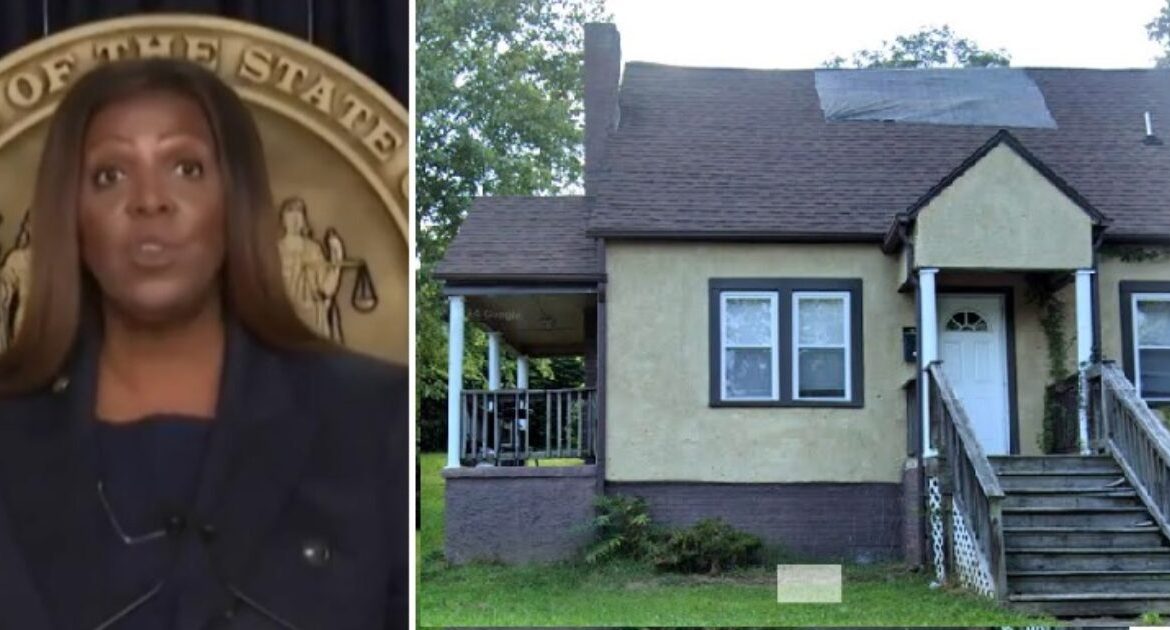

Letitia repeatedly told banks and the US government that her apartment building at 296 Lafayette Avenue in Brooklyn only had four apartment units, when in fact the official Certificate of Occupancy for her building indicates it had five.

The significance is that Letitia qualified for lower interest residential rates with only four units, while five-apartment units are assigned higher commercial rates. In addition, James obtained a government HAMP loan that was not even vailable to borrowers with more than four units.

Separate from the Brooklyn building, Sam Antar has documented, on his. website White Collar Fraud, that Letitia James claimed that a home she purchased in Norfolk, Virginia, would be her primary residence, a designation that also garners more favorable loan terms from banks.

Bill Pulte, Director of the Federal Housing Finance Agency, sent a criminal referral to the US Justice Department citing these problems in Letitia James’s mortgage history.

Now scrutiny is shifting to insurance fraud.

Firstly, this regards James’s claim of residence for a home mortgage in Norfolk, Virgina. Whether a home is owner-occupied or not plays a significant role in how insurance companies determine rates for homeowners’ insurance.

Owner-occupied homes – the primary residence in which the homeowner actually lives – are typically considered lower risk by insurers. They believe that these home are better and regularly maintained and monitored, and that issues like water damage, fire, or theft are more likely to be caught early or prevented altogether.

As a result, insurance premiums for owner-occupied homes are generally lower. These policies often come with standard coverage packages, such as HO-3 policies, which include protection for the dwelling, personal property, liability, and loss of use.

In contrast, non-owner-occupied homes, such as rental properties, vacation homes, or vacant houses, pose a higher risk and usually come with higher premiums.

For rental properties, landlords need specialized insurance (often called DP-3 policies) that covers the dwelling, liability, and potential loss of rental income.

Since tenants may not maintain the property as carefully as a homeowner would, the risk of damage increases, leading to more expensive coverage.

Vacant homes are considered even riskier due to the potential for vandalism, theft, and undetected damage. These often require separate vacant home insurance policies with limited terms and elevated costs.

Ultimately, insurance companies base their rates on perceived risk. Whether or not a home is owner-occupied is a key factor in that calculation.

Regarding Letita James’s claim of only four units in her apartment building in Brooklyn, insurance policies for apartment buildings vary significantly based on the number of units, with a major distinction occurring between buildings with four or fewer units and those with five or more.

Properties with up to four units – such as duplexes, triplexes, or fourplexes – are typically treated as residential properties for insurance purposes. These buildings often qualify for standard residential insurance policies, such as a Dwelling Property (DP-3) policy or even a Homeowners (HO-3) policy if the owner occupies one of the units.

These residential policies are relatively straightforward, come with lower premiums, and usually include coverage for the building structure, liability, loss of rental income, and optional protection for items like appliances. Since these properties are smaller and often self-managed, insurance companies consider them lower risk.

In contrast, buildings with five or more units are generally classified as commercial properties and require a more expensive commercial property insurance policy. These larger buildings face greater risk due to the higher number of tenants, increased maintenance needs, and more complex liability exposure.

As a result, commercial insurance policies are more comprehensive and customizable, often including coverage for the building itself, general liability, loss of rental income or business interruption, equipment breakdown, ordinance or law compliance, and even crime or vandalism protection.

The underwriting process for these policies is more rigorous and may involve property inspections or detailed financial disclosures. Because of the higher risk and broader coverage, premiums for commercial apartment insurance are typically much higher.

In many cases, these properties are managed by professional firms rather than individual landlords. Understanding the difference between residential and commercial classification is essential for property owners to ensure they have the appropriate coverage to protect their investment.

By misrepresenting both the residency status for her Norfolk home, and the number of units in her Brooklyn apartment building, Letitia James may well have broken the law.

If an individual knowingly provides false information to an insurer, particularly during the claims process, the act may be classified as insurance fraud – a serious criminal offense.

Unlike minor errors or omissions, intentional misrepresentation is treated as a deliberate attempt to deceive the insurance company for financial gain. Insurance fraud can lead to significant legal consequences, including substantial fines, court-ordered restitution, and even jail time, especially in cases involving large claims or repeated offenses.

In many states, insurance fraud is prosecuted as a felony, carrying long-term consequences such as a permanent criminal record. Authorities take these cases seriously, and insurers actively investigate suspicious claims, often with the help of fraud detection units and industry databases.

Being convicted of insurance fraud not only results in legal penalties but can also destroy a person’s credibility and future insurability. As Ms. James reminded us repeatedly during her legal harassment of Donald Trump, no one is above the law, not even Letitia James.

Joel Gilbert, is a Los Angeles-based film producer, and president of Highway 61 Entertainment. He is on Twitter: @JoelSGilbert.

The post New in the Letitia Files: Did New York AG Letitia James Commit Insurance Fraud, Too? It Looks Like It appeared first on The Gateway Pundit.